Europe was downgraded but did that actually only finished the low for some time ?

Europe was bullish today where parrticulary companies who do export did rally.

Once again, the most strong gains were seen in Nordic Territory (the export territory).

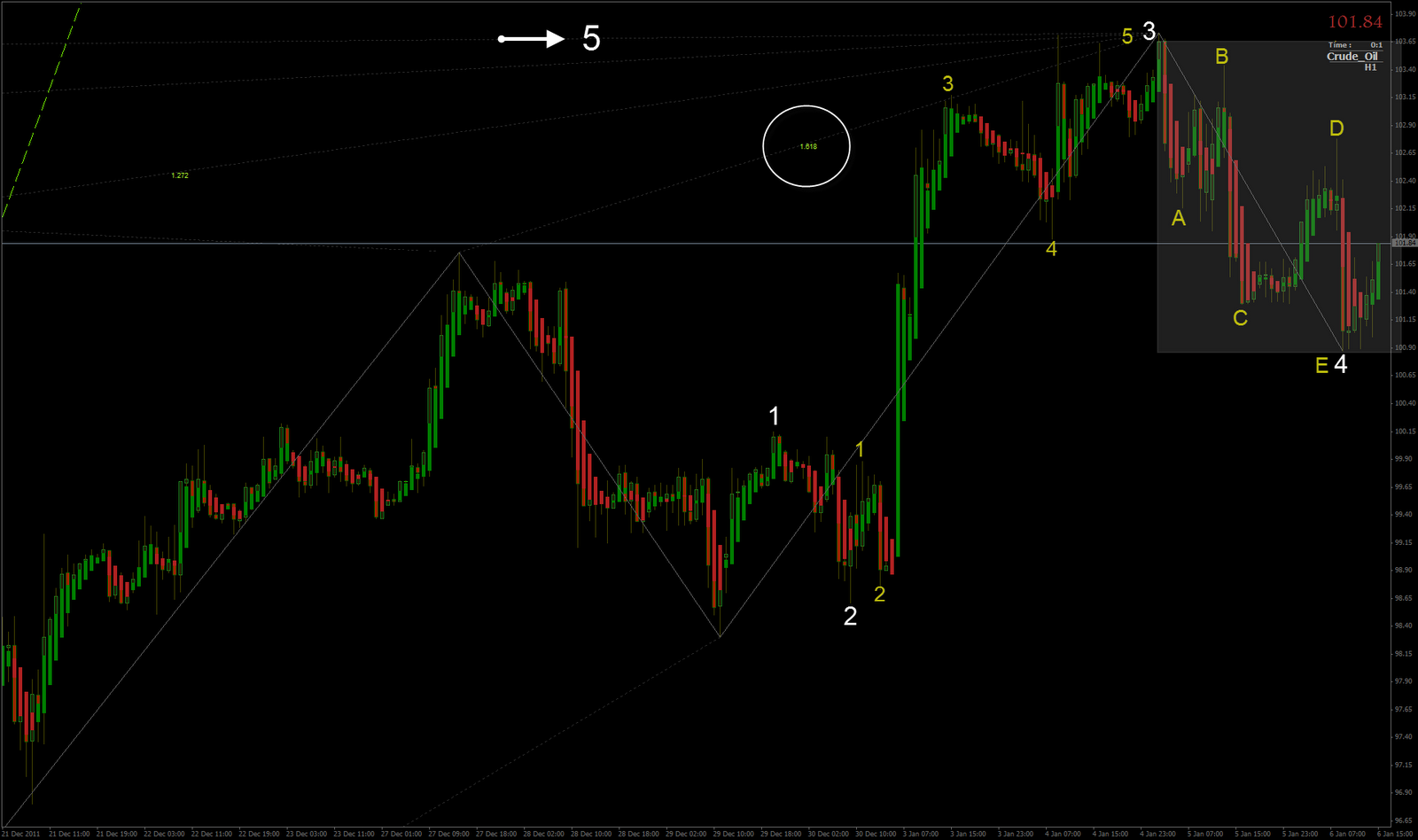

Uber busy week ahead in US to which I am entering with pretty neutral minds, I have MSFT but I am slightly carefull with Intel, it looks a toppy for me as 5 five.

Earnings Expectations for the Week of January 16th, 2012

Wells Fargo

When this San Francisco-based lender releases its fourth-quarter results Tuesday morning, it is expected to say that earnings rose from $0.61 per share a year ago to $0.72. That estimate has not changed over the past 60 days. And for the full year, analysts expect earnings to have risen 21.6% to $2.82 per share. Note that Wells Fargo earnings have not fallen short of consensus estimates in the past ten quarters. In the three months that ended in December, Wells Fargo completed conversion of its remaining Wachovia branches, and it was voted number one in customer satisfaction. Revenues for the fourth quarter, however, are predicted to have decreased 6.6% to $20.1 billion, and to have fallen 5.4% for the full year to $80.6 billion. The share price is up almost 15% in the past month, rising above resistance at $27 it had faced since August. The stock has outperformed peers Bank of America, Citigroup and JP Morgan over the past six months.

Goldman Sachs

Analysts are looking for this New York bank to report Wednesday morning that its per-share earnings declined 67.3% year over year to $1.24. And full-year earnings are forecast to have fallen 63.3% to $4.84 per share. Both EPS forecasts have been falling over the past 90 days. And for the fourth quarter during which the company expanded the number of its board members, revenues are expected to total $6.5 billion. That would be a 24.3% decrease from a year ago. Full-year revenues are expected to have fallen 23.1% to $30.1 billion. Note that Goldman’s earnings fell short of estimates in the previous two quarters, after topping them in the three quarters before that. The share price is up 5.9% in the past week but still 41.6% lower than a year ago. Over the past six months, the stock has underperformed competitors Citigroup and JP Morgan and the broader markets.

Morgan Stanley

During the three months that ended in December, this financial holding company reached a settlement with MBIA (NYSE:MBI) over mortgage-backed securities and announced the sale of Saxon Mortgage Services. On Thursday morning, Morgan Stanley is expected to post a net loss of $0.57 per share and revenues of $5.6 billion for that period. That compares to $0.43 per share earnings and $7.8 billion in the year-ago quarter. Analysts also expect full-year EPS to have fallen 66.4% to $0.82 per share and revenues to be up 2.8% to $32.5 billion. Both fourth-quarter and full-year EPS estimates have been falling over the past 60 days. But analysts have underestimated Morgan Stanley’s earnings results in the past four quarters. The share price has increased 9.6% in the past month, but it is still 40.7% lower than a year ago. And over the past six months, the stock has just managed to outperform competitor Goldman Sachs.

Here’s quick rundown of what analysts expect for earnings from some of the many banks and other financial firms reporting quarterly results this week.

* American Express (NYSE: AXP): EPS up 10.2% to $0.98 (reports Thursday)

* Bancfirst (NYSE: BANF): EPS down 2.7% to $0.73 (reports Tuesday)

* Bank of America (NYSE: BAC): EPS up 82.6% to $0.23 (reports Thursday)

* Bank of New York Mellon (NYSE: BK): EPS down 10.2% to $0.53 (reports Wednesday)

* Bank of the Ozarks (NYSE: OZRK): EPS down 0.2% to $0.49 (reports Tuesday)

* BB&T (NYSE: BBT): EPS up 43.3% to $0.53 (reports Thursday)

* Blackrock (NYSE: BLK): EPS down 11.9% to $3.01 (reports Tuesday)

* Capital One Financial (NYSE: COF): EPS up 1.9% to $1.55 (reports Thursday)

* Charles Schwab (NYSE: SCHW): EPS up 23.1% to $0.13 (reports Wednesday)

* Citigroup (NYSE: C): EPS up 18.4% to $0.49 (reports Tuesday)

* City National (NYSE: CYN): EPS up 10.8% to $0.83 (reports Thursday)

* Comerica (NYSE: CMA): EPS down 11.3% to $0.47 (reports Friday)

* Community Trust Bancorp (NYSE: CTBI): EPS up 7.7% to $0.65 (reports Wednesday)

* Fifth Third (NYSE: FITB): EPS up 8.3% to $0.36 (reports Friday)

* First Horizon National (NYSE: FHN): swings from a year-ago loss to $0.14 EPS (reports Friday)

* First Republic Bank (NYSE: FRC): EPS up 9.1% to $0.66 (reports Tuesday)

* Huntington Bancshares (NYSE: HBAN): EPS up 64.3% to $0.14 (reports Thursday)

* M&T Bank (NYSE: MTB): EPS down 8.2% to $1.46 (reports Tuesday)

* Northern Trust (NYSE: NTRS): EPS up 13.2% to $0.68 (reports Wednesday)

* People’s United Financial (NYSE: PBCT): EPS up 47.4% to $0.19 (reports Thursday)

* PNC Financial Services (NYSE: PNC): EPS down 6.0% to $1.41 (reports Wednesday)

* Prosperity Bancshares (NYSE: PB): EPS up 7.9% to $0.76 (reports Friday)

* SLM (NYSE: SLM): EPS down 34.7% to $0.49 (reports Wednesday)

* State Street (NYSE: STT): EPS up 7.4% to $0.94 (reports Wednesday)

* Suntrust Banks (NYSE: STI): EPS up 14.8% to $0.27 (reports Friday)

* US Bancorp (NYSE: USB): EPS up 22.2% to $0.63 (reports Wednesday)

* WestAmerica BanCorp (NYSE: WABC): EPS down 2.5% to $0.79 (reports Thursday)

Of course, it will not only be financial companies reporting this week. Here is quick look at what analysts estimate for earnings in just a few of the most prominent of this week’s other quarterly reports.

* eBay (NYSE: EBAY): EPS up 8.8% to $0.57 (reports Wednesday)

* Freeport McMoRan Copper & Gold (NYSE: FCX): EPS down 60.7% to $0.64 (reports Thursday)

* General Electric (NYSE: GE): EPS up 7.9% to $0.38 (reports Friday)

* Google (NASDAQ: GOOG): EPS up 16.5% to $10.48 (reports Thursday)

* IBM (NYSE: IBM): EPS up 9.5% to $4.62 (reports Thursday)

* Intel (NYSE: INTC): EPS up 3.3% to $0.61 (reports Thursday)

* Microsoft (NASDAQ: MSFT): EPS down 1.3% to $0.76 (reports Thursday)

* Schlumberger (NYSE: SLB): EPS up 22.0% to $1.09 (reports Friday)

* Southwest Airlines (NYSE: LUV): EPS down 87.5% to $0.08 (reports Thursday)

* Union Pacific (NYSE: UNP): EPS up 13.8% to $1.81 (reports Thursday)

* UnitedHealth Group (NYSE: UNH): EPS down 1.9% to $1.03 (reports Thursday)